I first wrote about the increasing domination Facebook, Apple, Microsoft, Google, and Amazon (aka FAMGA) in January of this year. It was not a particularly widely read piece. But every day since then, I’ve become surer of the simple, but profoundly impactful, realization that:

- The most valuable companies in the U.S. are increasingly tech companies

- The concentration of value (as denoted by market cap) being created in tech, is increasingly being created by the five largest companies, Facebook, Apple, Microsoft, Google and Amazon (a.k.a. FAMGA)

- The concentration of market cap in just five hands will have an increasingly profound impact on innovation and wealth concentration in the U.S..

So I’ll keep beating the FAMGA drum.

FAMGA By The Numbers

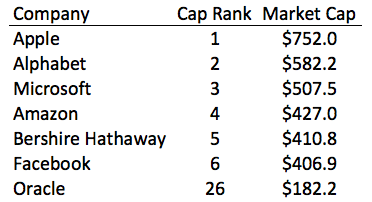

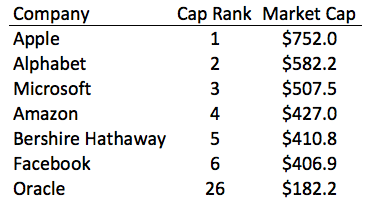

As of Friday, April 7th , FAMGA stocks finished with an average market cap of $535 billion. The smallest FAMGA market cap is Facebook, at $407 billion. Number six in terms of market cap in U.S. tech land is Oracle at at $182 billion, just 45% of the market cap of Facebook. So there is massive, and growing, separation between FAMGA and the rest of tech in terms of market cap:

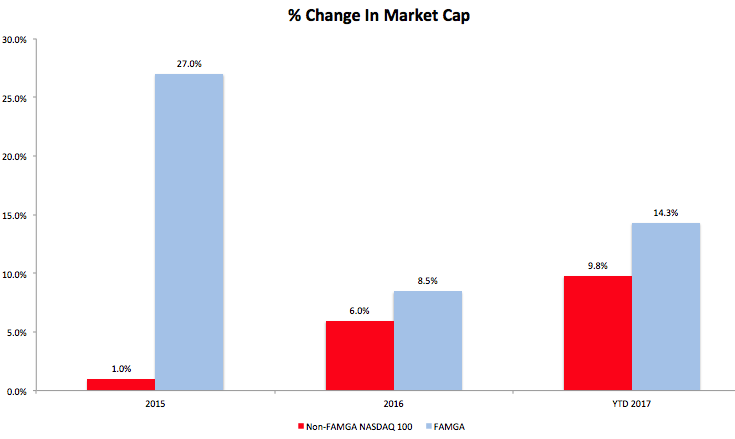

FAMGA continues to outperform the non-FAMGA stocks in the NASDAQ 100 in 2017

The FAMGA stocks have had a great run the last two years, and that trend has continued so far in 2017, continuing to outpace the performance of the 95 non-FAMGA NASDAQ 100.

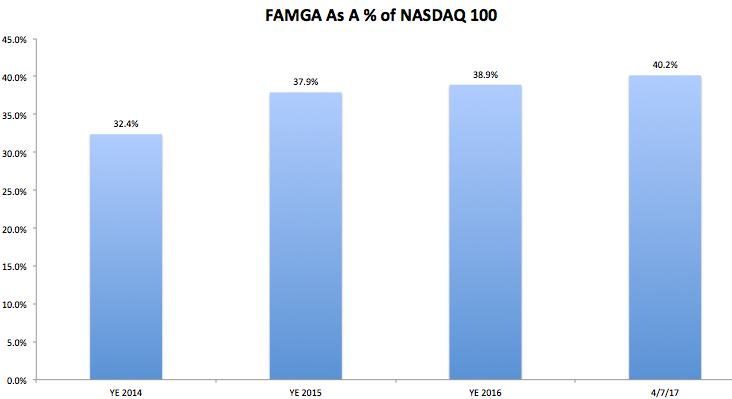

As a result of the outperformance of FAMGA relative to the non-FAMGA stocks in the NASDAQ 100, the percentage of the total market cap of the NASDAQ 100 that is comprised of FAMGA market cap, has continued to grow:

The Implications Of The FAMGA Market Cap Concentration

Innovation Slows In Monopolies/Duopolies

I’m not saying FAMGA are doing anything wrong. They are simply all great competitors benefitting from the “winner, or two winners, take all” markets that increasingly comprise most digital markets (and almost all markets are going digital).

Take the internet advertising market. The good news is that according to the Internet Advertising Bureau (IAB), internet advertising was up 20% year-ver-year in 3Q ’16. The bad news is that, if you take FAMGA out of the equation, internet advertising revenue probably shrank for everyone else:

The analysis above groups Amazon in to the “Everyone Else” category. Given that Amazon is estimated to have generated around $1 billion in advertising revenue, it’s likely that Amazon grew it’s advertising revenue by more than $40 million Q3 16 v Q2 ’16. The point is, that taking FAMGA out of the equation, the market is actually shrinking. What happens in shrinking markets? Innovation is stifled due to lack of competitive reasons to innovate, and due to lack of resources. CBInsights reported that global ad tech funding fell 33% in 2016 to $2.2 billion, from $3.2 billion in 2015, putting it back to where it was in 2013. That decrease is innovation withering in the ad tech market.

E-commerce is in the U.S. is increasingly being dominated by Amazon, which accounted for 53% of all e-commerce revenue growth in 2016, bringing it’s growing control of the e-commerce market to 43% share. Funding to e-commerce companies fell over 44% in 2016 to $9 billion according to CBInsights. That’s a lot less capital funding innovation in e-commerce.

Adjacent Markets Become Ripe For Domination

Software is increasingly eating the world. Technical superiority is increasingly the largest factor in who dominates different markets. Then it makes sense that FAMGA will increasingly dominate other markets.

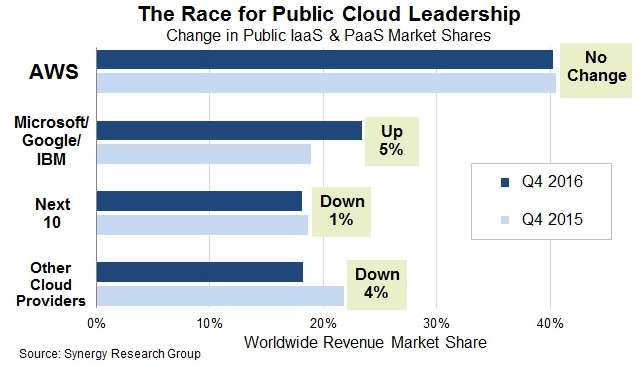

One obvious example of this premise is the public cloud space, where Amazon dominates:

Amazon has roughly the same dominant global market share in the pubic cloud space as it does in U.S. e-commerce. Other FAMGA members, Google and Microsoft (along with IBM) are gaining share, and everyone else is losing.

Other Implications/Thoughts

There are numerous other important implications to consider, but I’’m going to write about three now, and save the rest for future FAMGA drumbeats.

First, it’s not just adjacent markets that are ripe for domination by FAMGA, it’s any new market with large potential that takes large amounts of capital and technical expertise. Think about AR/VR (Facebook). Think about the race to space (Amazon). Think about self driving cars (Google). Now each of those areas have significant other competitors, but I believe FAMGA are well positioned to take dominant share in each of those markets.

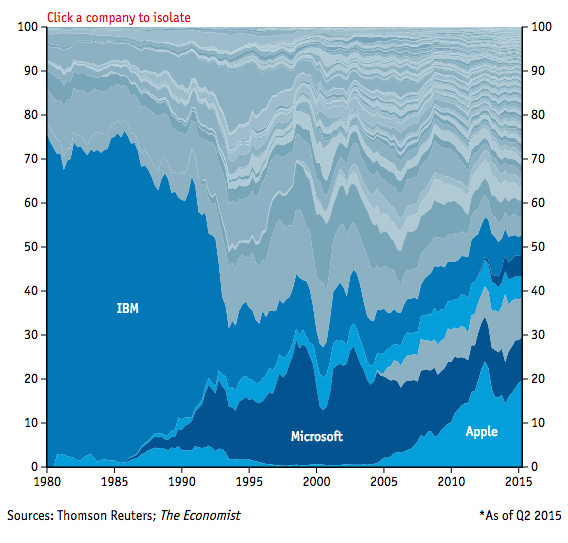

Second, we’ve been here before. Below is one of my favorite all time charts. It shows the market cap market share of the 100 most valuable tech companies in the U.S., over time:

In 1985, IBM controlled over 70% of the total market cap of the 100 largest U.S. tech companies. In 1998 Microsoft controlled 30% of the total market cap, and we were worried that Microsoft was stifling of innovation. In 2012, Apple controlled over 25% of the market cap. Google was the largest market cap for 42 hours last year. History has taught us that nothing is constant but change.

Finally, simultaneous with the rise of FAMGA, the pace of innovation is accelerating, and there are a huge number of companies creating massive shareholder value through innovation. Just last week, Tesla surpassed Fordin market cap, at $49.3 billion. Tesla is now worth just 2% less than GM. Netflix is worth $60 billion. Uber is worth $66 billion. Intel just bought Mobileye for $15 billion. AirBnB is worth $30 billion.

So there are lots of competing forces at play here. It turns out, this is complex (who knew?). But the forces compelling FAMGA to ever greater share of market cap are strong, and as it continues, the implications will be increasingly profound.