Recently, Innovention, one of three non-profit Incubators operated by New York University, held a discussion on the legal and fundraising aspects of startups. The organization strives to help students and entrepreneurs stay on the right path and avoid common mistakes when starting a business – mistakes that would save entrepreneurs time and money along the way.

The 5 common legal pitfalls that founders find themselves in are:

- Forming an entity at value.

Instead, when you’re forming a company, form it at no value. This way, there is a limited liability. By building value outside of an entity at the beginning, there is no disparity in value. Forming a company as early as possible at no value allows the value to build throughout.

Also, forming a company allows for limited liability: in the event that a product malfunctions, the company is sued, not the individual. When faced with the decision to choose an LLC or a corporation, tech companies should consider being a corporation. Very few angel investors invest in LLCs.

- Not agreeing on equity.

Equity does not stay the same – it changes throughout. Founders should figure out their company’s equity early on to avoid misunderstandings down the road. Sign restriction agreements at the beginning.

- Not signing Stock Restriction Agreements.

What a lot of entrepreneurs don’t realize is that when you found a company with other people and they own, for example, fifty percent of the company shares, in the event that a founder leaves down the road, they can take that fifty percent with them. Signing a Stock Restriction Agreement prevents them from taking that fifty percent from the company.It also means that the company can buy back that share during a period of time, until everyone has fully invested. This usually takes 2-4 years.

Do not forget to file for 83B after restricting your stock. This means that when you pay the fair market value on all your stock today, you will not be taxed on those stocks again until you sell it.

- Forgetting to sign an Invention Assignment Agreement with all the founders.

This is an agreement that states that the products that an individual created for the company is owned by the company. So, in the event that the creator leaves, the company still owns the IP.

- Misclassifying interns, employees, and consultants.

Interns can be considered as consultants.If you are unsure how to classify your workers, seek out the advice of a lawyer or an adviser. Avoid misclassifying your workers, or you will receive a visit from the Department of Labor.

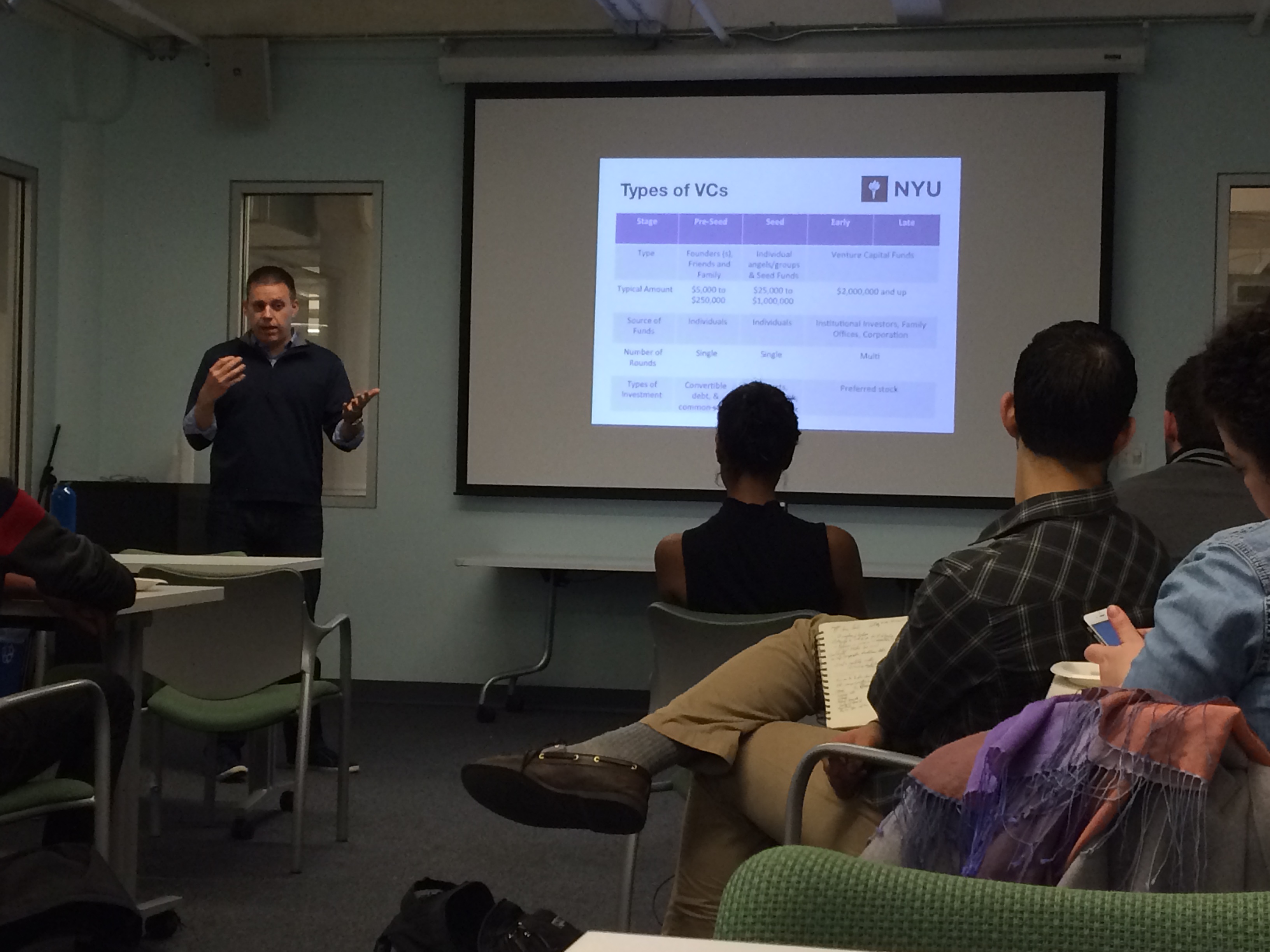

When it comes to fundraising for capital for your startup, timing is most important. Also, entrepreneurs have to remember these 5 tips:

- Know the key players.Entrepreneurs have their co-founders and their lawyers. In addition, there are:

The Venture Capitalists: Talk to senior and mid-level VCs. For example, Managing Directors or General Partners.

Angel Investors: They must be accredited investors. Always ask for references. Also, be wary of having friends and family invest in your company.

Mentors: Angel investors make good mentors, but they should not be brokering deals for you. Mentors are usually uncompensated, but if you must, do not go higher than 50%.

- Find a lead investor. They will set the term for the rest of the deal. Try to close around funding as quickly as possible and don’t wait too long.

- Prepare important documents before you need them.

This includes:

Capitalization Tables

Contracts

Material Agreements

Employment Agreements

Board Minutes

- Know your investors.

Establish a relationship with them before you even pitch your idea.

- Don’t wait until you need money to start fundraising.

Be prepared for the inevitable.

Beginning a company has no shortcuts and mistakes are inevitable. However, you want to avoid wasting time and money on mistakes that are easily avoided. Remember these tips and you will be good to go on creating a successful company.