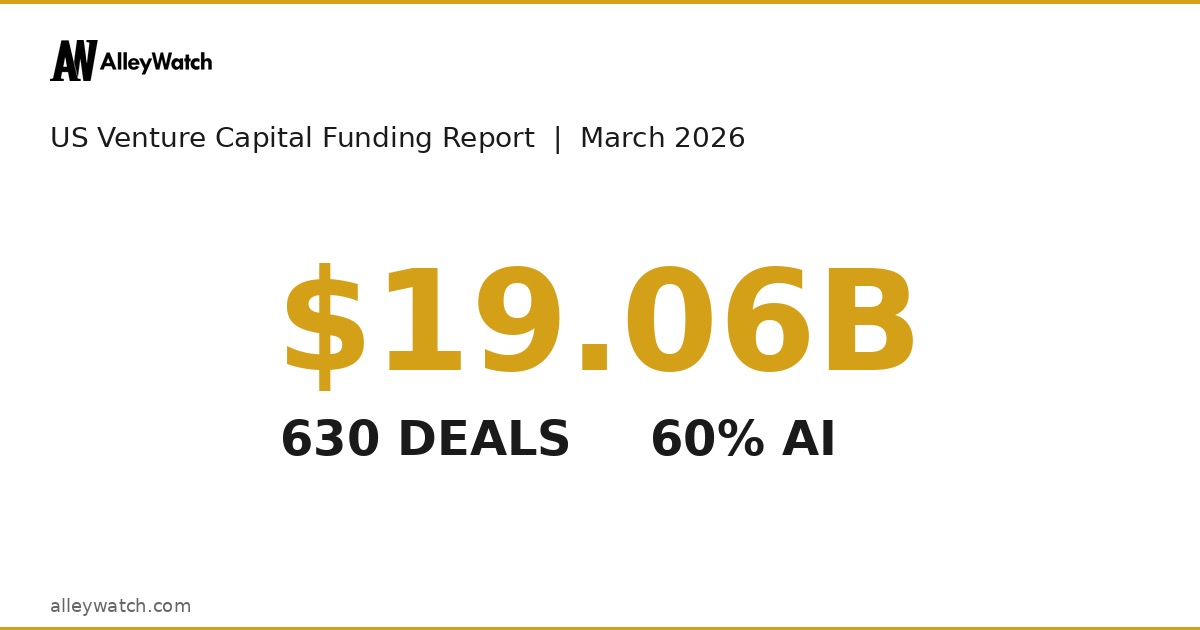

US startups raised $19.06 billion across 630 deals in March 2026, a figure that reflects market normalization following the anomalous mega-rounds that defined early 2026. Compared to March 2025’s $53.5B total — itself inflated by OpenAI’s $40B raise — the headline decline of 64.4% masks a more stable underlying market. Strip out OpenAI from last year’s comparison and the market is down 28.9%.

🔑 Key Insights

- $19.06B raised across 630 deals in March 2026 — down 64.4% YoY from March 2025’s $53.5B, but that figure included OpenAI’s $40B mega-round.

- The market declined 69.5% month-over-month from February 2026’s $62.54B, which was anchored by Anthropic’s $30B and Waymo’s $16B — signaling a return to pre-mega-round baseline activity.

- AI companies captured 60.1% of all US venture capital ($11.46B across 316 deals), underscoring the sector’s continued dominance even absent frontier model mega-rounds.

- Shield AI ($2.0B) and Saronic ($1.75B) led the month with massive late-stage raises in autonomous defense systems, reflecting investor conviction in AI-powered military and maritime applications.

- Late-stage rounds captured 46.7% of capital ($8.91B across 45 deals), with an average deal size of $197.9M reflecting concentration in proven, scaling companies.

- Geographic distribution showed strength beyond traditional hubs: NYC (20.7%), San Diego (11.3%), Austin (10.4%), and Palo Alto (10.5%) captured significant share alongside San Francisco (10.1%).

- The median deal size of $6.0M and average of $37.0M reflect a two-tiered market: robust seed/Series A activity at the base and mega-round concentration at the top.

US Startup Funding — March 2026

March’s figures must be contextualized against the extraordinary mega-rounds that defined the prior two months. February 2026’s $62.54B was lifted almost entirely by Anthropic’s $30B and Waymo’s $16B — the two largest venture rounds ever recorded. March 2025’s $53.5B included OpenAI’s $40B, which alone exceeded March 2026’s entire total. Strip those outliers from comparison and the market appears stable: the $19.06B raised in March 2026 sits comfortably within the $15B–$25B monthly range that characterized most of 2024 and 2025.

The month’s capital was concentrated at the extremes. Shield AI’s $2 billion late-stage round for autonomous defense systems and Saronic’s $1.75 billion raise for AI-powered maritime platforms together accounted for nearly 20% of the month’s total. These mega-rounds reflect a specific investor thesis: AI-enabled national security and defense applications command premium valuations in an era of geopolitical tension. Beyond defense, WHOOP ($575M), Sierra Space ($550M), and consumer brands like Quince ($500M) demonstrated that non-AI categories can still command significant late-stage capital when business models are proven and scaling trajectories are clear.

US Funding by Round Type — March 2026

| Round Type | # Deals | Capital Raised | % of Total $ | Median Deal | Avg Deal |

|---|---|---|---|---|---|

| Early-Stage | 317 | $1.43B | 7.5% | $2.0M | $4.5M |

| Series A | 108 | $4.79B | 25.1% | $23.9M | $44.4M |

| Series B | 45 | $3.92B | 20.6% | $42.0M | $87.2M |

| Late-Stage | 45 | $8.91B | 46.7% | $60.0M | $197.9M |

| Total | 515 | $19.06B | 100% | $6.0M | $37.0M |

The stage distribution reveals a market driven by late-stage concentration. Late-stage rounds captured 46.7% of capital despite representing just 8.7% of deal count, with an average deal size of $197.9M. This reflects investor preference for companies with demonstrated traction and clear paths to profitability or exit. Series A and Series B rounds combined for $8.71B (45.7% of total capital), signaling healthy mid-funnel activity as companies progress from product-market fit into scaling mode.

Early-stage activity, while accounting for 61.6% of deal count (317 deals), captured just 7.5% of capital ($1.43B). The median early-stage deal of $2.0M and average of $4.5M indicate a seed market that remains active but capital-constrained relative to growth stages. This pattern is consistent with a venture environment where later-stage capital abundance has not trickled down uniformly to the earliest stages.

Top 10 US Venture Capital Deals — March 2026

| # | Company | Amount | Round | Sector |

|---|---|---|---|---|

| 1 | Shield AI | $2.00B | Late-Stage | Artificial Intelligence (AI), Autonomous Vehicles, Drones, M |

| 2 | Saronic | $1.75B | Late-Stage | Artificial Intelligence (AI), Manufacturing, Marine Technolo |

| 3 | WHOOP | $575M | Late-Stage | Consumer Electronics, Fitness, Sports, Wearables, Wellness |

| 4 | Sierra Space | $550M | Late-Stage | Advanced Materials, Aerospace, Industrial Manufacturing, Spa |

| 5 | Quince | $500M | Late-Stage | Apparel, E-Commerce, E-Commerce Platforms, Retail |

| 6 | Mind Robotics | $500M | Series A | Artificial Intelligence (AI), Machine Learning, Robotics |

| 7 | Nexthop AI | $500M | Series B | Artificial Intelligence (AI), Cloud Data Services, IT Infras |

| 8 | Rhoda AI | $450M | Series A | Artificial Intelligence (AI), Business Intelligence, Foundat |

| 9 | Replit | $400M | Late-Stage | Artificial Intelligence (AI), Cloud Computing, Developer Too |

| 10 | Genspark | $385M | Series B | Artificial Intelligence (AI), Generative AI, Machine Learnin |

AI Sector Dominance

AI companies raised $11.46B across 316 deals in March 2026, representing 60.1% of total capital and 50.2% of deal count. This marks a sustained majority even without the frontier model mega-rounds (Anthropic, OpenAI) that characterized prior months. The capital is flowing to applied AI infrastructure, autonomous systems, and vertical AI solutions rather than foundational model development.

Defense and autonomous systems commanded the largest checks: Shield AI ($2.0B) for defense autonomy, Saronic ($1.75B) for maritime AI, and Mind Robotics ($500M Series A) for robotics. Enterprise AI infrastructure also attracted significant capital, with Nexthop AI ($500M Series B), Rhoda AI ($450M Series A), Replit ($400M), and Genspark ($385M) all closing nine-figure rounds. The pattern is clear: AI remains the dominant investment theme, but the capital is shifting from foundational models to application layers and deployment infrastructure.

Geographic Distribution

| City | Capital Raised | Deals | % of US Total |

|---|---|---|---|

| New York | $3.94B | 97 | 20.7% |

| San Diego | $2.15B | 8 | 11.3% |

| Palo Alto | $2.01B | 14 | 10.5% |

| Austin | $1.98B | 17 | 10.4% |

| San Francisco | $1.92B | 83 | 10.1% |

| Santa Clara | $680M | 4 | 3.6% |

| Boston | $650M | 7 | 3.4% |

The standout geographic story is San Diego’s 11.3% share ($2.15B across just 8 deals), driven almost entirely by Saronic’s $1.75B raise for maritime autonomous systems. This single deal demonstrates how mega-rounds can temporarily reshape geographic rankings. Austin’s 10.4% ($1.98B across 17 deals) reflects broader ecosystem momentum in Texas as companies increasingly choose the city for its talent, cost structure, and regulatory environment.

Palo Alto (10.5%) and San Francisco (10.1%) — the traditional Bay Area hubs — captured a combined 20.6% of national capital, a notably smaller share than historical norms where Silicon Valley routinely commanded 35–40% of venture deployment. New York’s 20.7% ($3.94B across 97 deals) continues the city’s pattern of securing an outsized share of national capital, particularly in financial services, healthcare, and enterprise infrastructure — as detailed in AlleyWatch’s separate NYC-specific March 2026 funding report.

Stay Ahead of US Tech & Venture Capital

Join 100K+ Email List Contacts receiving insights on US startup funding, VC trends, and market analysis.

Methodology

All data sourced from Crunchbase. Deal counts and funding totals reflect announced and disclosed venture capital transactions with a last funding date in March 2026. Round type classifications follow a standardized four-category taxonomy: Early-Stage (pre-seed through seed), Series A, Series B, and Late-Stage (Series C and beyond, including growth and corporate rounds). AI company identification was applied using pattern matching across company descriptions, industry tags, and organization names. Year-over-year comparisons reference March 2025 figures of $53.5B. Month-over-month comparisons reference February 2026 figures of $62.54B across 462 deals. Classified totals exclude 177 deals categorized as “Unclassified” due to insufficient round type data. Geographic analysis based on headquarters location as reported in Crunchbase.

AlleyWatch and Alumni Ventures are teaming up this week only to give readers early access to high-growth startup opportunities, including some of today’s most exciting AI, Deep Tech, Quantum Computing, Cybersecurity, and Space companies co-invested alongside top VC firms like Andreessen Horowitz (a16z), Bessemer, & Y Combinator.

You get:

- Curated deal flow of high-potential startups

- AV is already investing alongside elite lead venture firms in these deals

- No cost to see deals

- No obligation to invest

Don’t miss your chance before access closes.

Data sourced from Crunchbase.